No items found.

Free Webinar · May 7 · How to Get (and Keep) More Patients as a Practitioner →

Save Your Spot

Table of Contents

Experience Better Practice Management Today!

Starting at $28.05/month

No Credit Card Required

Experience Better Practice Management Today!

Starting at $30/month

No Credit Card Required

Starting a clinic with another therapist feels exciting. You split costs, share the workload, and build something together. But partnerships get complicated fast, even with people you trust completely.

I've watched too many practitioner partnerships fall apart over simple disagreements that could have been prevented. That's why you need solid legal agreements before you start treating patients.

In this post, I'll explain why a shareholders' agreement is critical for your clinic partnership. Here's what we'll cover:

Sort these details out early and you'll avoid messy conversations later. Let me show you what makes an effective shareholders' agreement.

After a decade of working with practitioners, I know one thing for sure: handshake deals don't work. A shareholders' agreement is a written contract that defines how your business operates with multiple owners.

If your clinic is incorporated and you share ownership, this document covers ownership percentages, individual roles, and decision-making processes. It's your business playbook.

For partnerships that aren't incorporated, you need a partnership agreement instead. Same purpose, different structure.

Your agreement must address what happens during tough times, when someone wants out, or when you can't agree on clinic direction. These situations will happen. The question isn't if, but when.

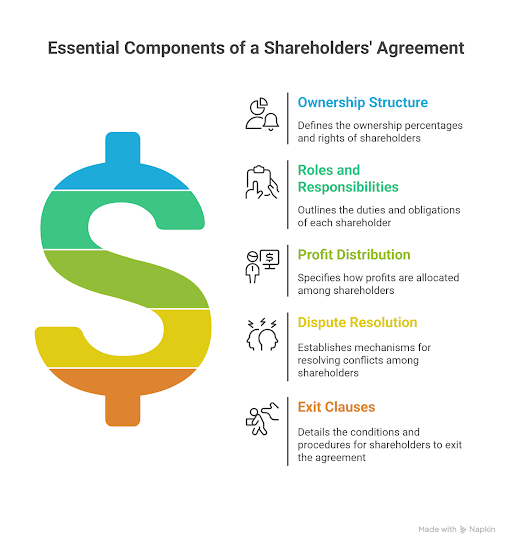

Now let's break down what your shareholders' agreement actually needs to include. These aren't just legal formalities. They're what keep your partnership running smoothly when things get complicated.

Your ownership split determines who controls what in your business. A 50/50 split sounds fair, but I've seen it cause problems. What if one partner brings in twice as many clients? What if someone puts in more money upfront?

I always tell clinic owners to think beyond equal shares. You could split based on financial investment, client generation, or hours worked. The key is deciding this before you open your doors, not after someone feels they're doing more work.

Get specific about voting rights, too. Some decisions need unanimous agreement, others don't. Define what both partners must agree on and what one person can decide alone.

You need clear job descriptions from the very beginning. I've watched partnerships crumble because both people tried to do everything, or worse, both thought the other person was handling something important.

Decide who will manage staff, handle finances, deal with insurance companies, and oversee patient care protocols. Write it down. When your clinic grows and you need to hire help, you'll know exactly who's responsible for what.

Don't make everything a joint decision. It slows you down and creates unnecessary friction.

Money ruins partnerships faster than anything else. Your agreement needs to outline clearly how you'll split the profits.

Equal splits work if you're contributing equally. But what if one partner works part-time while the other works full-time? What if someone's bringing in significantly more revenue?

I recommend tying profit distribution to actual contribution, whether that's time, money invested, or clients brought in. Make the formula clear and measurable. No room for interpretation means no arguments later.

You will disagree with your partner. It's guaranteed. The question is how you'll handle it when it happens.

Most of my successful partnerships use a simple escalation process. First, you try to work it out between yourselves. If that fails, you bring in a neutral mediator. As a last resort, you go to arbitration.

Skip the court system if you can. It's expensive, time-consuming, and usually destroys any chance of maintaining a working relationship.

This is the part nobody wants to talk about, but it's the most important: Partners leave. Sometimes, it's planned, and sometimes, it's sudden.

Your exit clause needs to cover how you'll value the business, who gets first right to buy out the leaving partner, and what happens if you can't agree on a price. Set the timeline too. How much notice is required?

I always include what happens if a partner becomes disabled, dies, or loses their professional license. These scenarios feel uncomfortable to discuss, but they protect everyone involved.

Don't wait to create your shareholders' agreement. Too many partnerships struggle because they put this off until problems start.

Create the agreement as soon as you decide to work together. I mean it - before you sign a lease, hire anyone, and see your first patient.

It's easy to agree on terms when everything's going well and you're both excited about the future. Wait until you're stressed about money or arguing about workload, and suddenly every conversation becomes a negotiation.

The early days feel simple, but they won't stay that way. Decisions get more complicated once you start treating patients, managing staff, and dealing with insurance companies.

Without an agreement, you'll make essential choices under pressure. That's when mistakes happen and resentment builds.

Don't draft the agreement until you've figured out the big picture. What's your clinic's focus? How do you want to grow? What are each person's strengths?

First, get alignment on these major points. Then put everything in writing. Your agreement should reflect how you want to run the business, rather than a generic template.

If your clinic is already running and you're considering expanding, adding partners, or offering new services, update your agreement now.

Growth changes everything: more revenue, more decisions, more complexity. Make sure your agreement covers how you'll handle these changes before they happen.

Even if you completely trust your partner, business partnerships can get complicated. A shareholders’ agreement is not just a piece of paper. It protects your clinic and your relationship.

Beyond the key elements of a shareholders’ agreement, there are some extra points you should think about to keep your partnership running smoothly.

Decide how the clinic’s taxes will be handled and clarify each partner’s responsibilities. Will you file as a sole proprietor, a corporation, or a partnership? Setting this up early prevents confusion and keeps your finances organized from day one.

A good agreement doesn’t just protect you today, it also supports your clinic’s growth. Whether adding new partners or expanding services, clear rules make transitions smoother.

Tools like Noterro can help with this by keeping scheduling, patient management, and billing consistent across multiple locations. This way, you and your partners can focus on growing the business without administrative headaches.

Segmenting patient files is essential when multiple practitioners work together. Noterro’s role-based permissions feature lets you control who can view notes. Assigning patients to specific practitioners and enabling “practitioner-only” access ensures that each person sees only their own notes.

This setup protects privacy and makes it simple to export files if a practitioner ever leaves the clinic.

Make sure confidentiality clauses are in place. This covers patient data, clinic practices, and any proprietary methods or branding. You should also decide upfront how intellectual property will be handled if the partnership changes. Clear rules here prevent disputes later.

I partnered with a fellow student in chiropractic college to open our first clinic. For the first three years, things ran smoothly. Then problems started to appear. Within two years, our relationship soured.

We had no shareholders’ agreement, and we hadn’t clarified ownership of patient files, clinic assets, or what would happen if one of us left. Conflicts over shared patients quickly became a legal battle over data, assets, and ownership.

Separating the clinic’s data and assets took five years and $250,000. A clear agreement from the start could have avoided all of this.

My advice is simple: put everything in writing. Partnerships change over time. A shareholders’ agreement and exit strategy protects you from costly disputes, lost opportunities, and unnecessary stress.

Partnering with another practitioner can build something great, but I've watched too many partnerships crash over simple issues that good agreements prevent.

A shareholders' agreement isn't just paperwork. It's what saves your partnership when disagreements happen. And they always happen.

Get your legal foundation right first. Define ownership, roles, and exit strategies before you need them.

Once that's sorted, tools like Noterro can handle scheduling, patient management, and billing while you focus on growing your practice. Protect your partnership and build something that lasts.

Tags

Nick Gabriele, Director, Noterro, has been leading the company to greater heights since May 2012. With his vision and 10+ years of expertise, Noterro has become a leading practice management software that offers users an innovative platform for storing notes, tracking appointments, and managing their practice.

Noterro was born out of the need to create a more efficient way to manage paper charts at Ontario College of Health and Technology, which Nick owned.

For nine years, he has performed Independent Medical Evaluations, which allowed him to sharpen his skills in assessing and providing solutions to various health-related issues. With a strong background in rehabilitation settings, including Chiropractic, Physiotherapy, and Massage Therapy, Nick has also garnered a wealth of experience in his field.

Furthermore, Nick has a knack for passion and proficiency in education that has also led him to work in private education for over 20 years. This invaluable experience has enabled him to develop a deeper understanding of how to deliver top-notch training and support to individuals and organizations alike.

In addition to his professional achievements, Nick is an active speaker and has participated in several webinars and podcasts on topics related to electronic record-keeping and practice management. He also has written a plethora of leadership articles on tech topics, including "Charting in the electronic age," "How to Leverage Practice Management Software." His work has been featured in top industry publications, such as Hamilton News. Nick’s insights also have been cited in notable Podcasts like Business Blueprint and Practiciology.

.webp)

No credit card required. Available 1-on-1 support.

.webp)

No credit card required. Available 1-on-1 support.

.webp)

.webp)

.webp)